Audit Management Letters a Guide for Churches

Understand audit management letters for churches. Learn to read findings, respond effectively, and prevent issues with true fund-based accounting.

You open the audit packet, scan the opinion, feel relieved for a moment, and then notice a second document sitting behind it. The title sounds formal. The wording feels sharp. Terms like “deficiency,” “control weakness,” and “recommendation” make it easy to assume something went badly wrong.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Start free to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That reaction is common, especially for a church treasurer, finance volunteer, or pastor who already carries a lot of responsibility. But an audit management letter usually isn't a failing grade. It's a working document. It points to places where your church can tighten processes, protect offerings, and document stewardship more clearly.

For churches, that matters at two levels. First, you want sound internal controls. Second, you have a deeper duty to honor donor intent, especially when gifts are restricted for missions, benevolence, a building project, or another designated purpose. That second piece is where many church leaders get tripped up.

Your Church Audit Is Done Now What

Sarah is a volunteer treasurer at a mid-sized church. She opens the audit packet, sees a clean opinion, and feels her shoulders drop. Then she turns the page, finds the management letter, and her stomach tightens again.

The language sounds formal and serious. Internal controls. Documentation. Segregation of duties. For a new treasurer, those terms can feel like a warning siren, even when the church has acted with integrity and carefully all year.

If that sounds familiar, pause here. A management letter usually means your auditor is pointing out places to tighten the process, document decisions better, and reduce future risk. It is a working paper for leadership, not a statement that someone failed morally or spiritually.

What this letter is really telling you

A management letter gives the board, finance committee, and staff a written list of issues the auditor wants leaders to address. Some items may be more serious, such as significant deficiencies or material weaknesses. Others are practical recommendations that would make accounting cleaner and oversight easier.

A simple way to read it is this: the auditor is showing you where your financial system has loose boards in the floor. The building is still standing, but a few areas need repair before someone gets hurt. In church finance, that “hurt” often looks like preventable confusion, weak documentation, or restricted money being reported unclearly.

For churches, that last part deserves special attention.

A finding about documentation or account setup is not only an operations problem. It can also affect your duty to track donor-restricted gifts accurately under current FASB presentation rules. If a missions gift, benevolence offering, or building contribution is not clearly supported and separated, the issue is bigger than bookkeeping. It touches stewardship, board oversight, and whether the church can show that restricted funds stayed in the right bucket.

Practical rule: Read the management letter like a repair list for your finance process, especially for any area connected to restricted funds.

Good records make that work much easier. If your auditor noted missing support, inconsistent approvals, or files that are hard to trace, review clear document retention guidelines for churches so your team knows what to keep and where to find it.

Why church leaders should pay attention now

The audit may be over, but the letter creates your next set of responsibilities. Board members need to know which findings affect controls in general and which ones could interfere with clean fund accounting for designated and donor-restricted gifts.

That distinction gets missed in many church audit conversations. A late bank reconciliation is a control issue. A restricted gift posted to the wrong fund or reported unclearly can become both a control issue and a compliance issue. Under newer financial statement presentation rules, churches need to show those categories clearly and consistently.

Strong follow-up also supports the church outside the audit room. If your church is growing, refinancing, or facing lender questions, clear records and credible oversight help build confidence around securing funding through proper auditing.

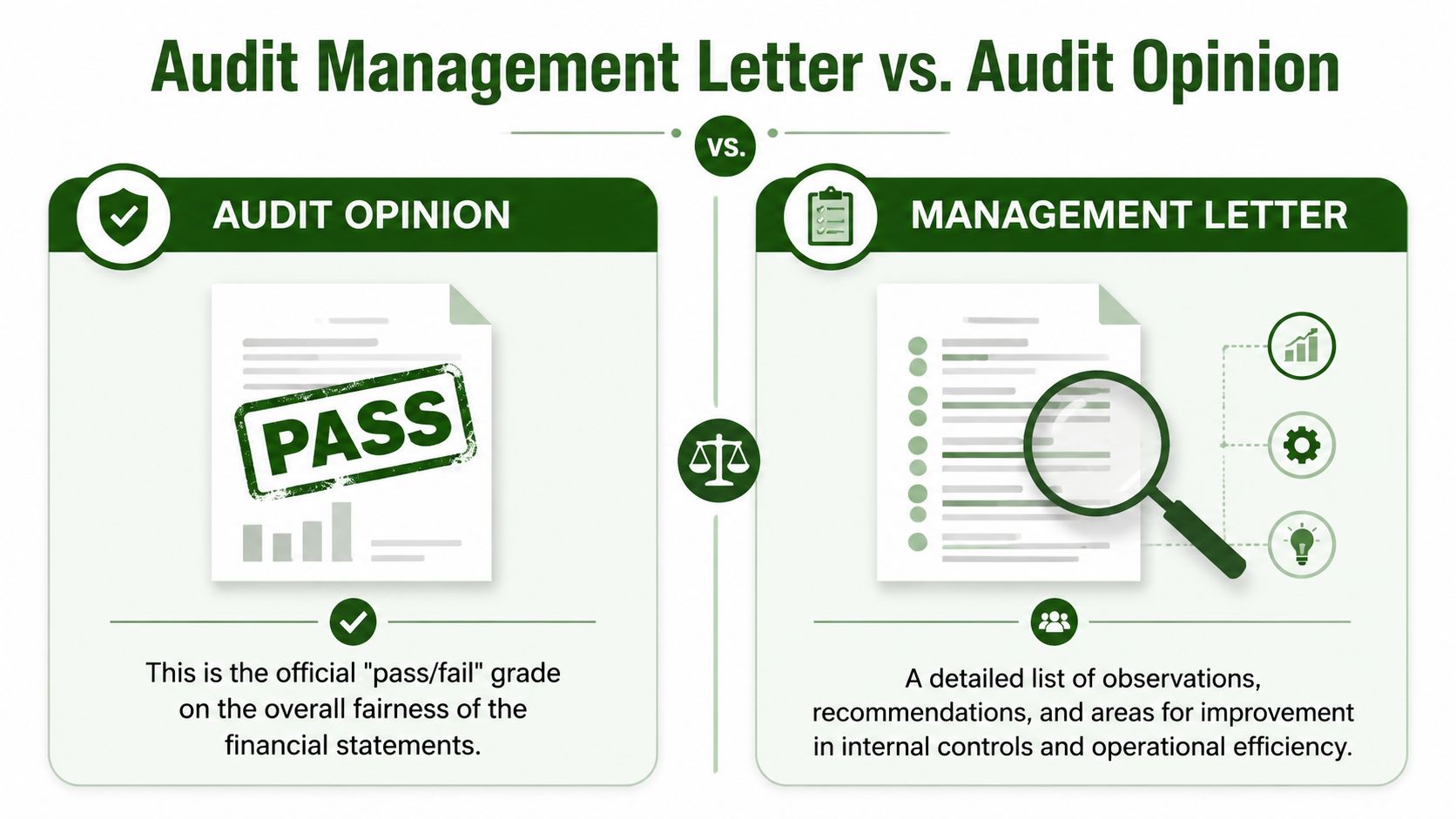

Management Letter vs Audit Opinion

Many church leaders treat the audit opinion and the management letter as if they were the same document. They're not. If you mix them together, the whole audit process feels more intimidating than it really is.

The simplest comparison is this. The audit opinion is the formal statement on whether the financial statements are presented fairly. The management letter is the auditor's written communication about weaknesses, risks, and improvements they want leadership to address.

Think house inspection, not report card

A clean audit opinion doesn't mean your church has perfect processes. It means the auditor believes the financial statements are fairly presented within the audit framework.

The management letter works more like an inspection report on the house itself. The house may be standing just fine, but the inspector still notes a loose handrail, a drainage problem, or an outdated panel. Those notes matter because they point to future risk.

Here's the contrast in plain language:

| Document | What it answers | Typical tone | What church leaders should do |

|---|---|---|---|

| Audit opinion | Are the financial statements fairly presented? | Standardized and formal | Read it for the overall opinion |

| Management letter | What control weaknesses or process issues need attention? | Specific and advisory | Review each point and assign action |

Why the management letter is formal

This letter isn't an optional extra when significant control issues are found. Audit management letters are legally mandated by international auditing standards (ASA 265) to formally communicate “significant deficiencies” and “material weaknesses” in internal controls in writing to those charged with governance, distinguishing them from the optional audit opinion. This cause-effect documentation is critical because a failure to communicate these deficiencies in writing constitutes a violation of professional standards, as explained in this discussion of management letters and ASA 265.

That matters for church boards because it explains why the language can feel so technical. The auditor is documenting a professional obligation. They need to be precise.

A management letter is often the most useful document in the audit packet because it tells leaders what to fix, not just what passed review.

What a well-written letter usually includes

Most audit management letters follow a practical pattern, even if they don't all look identical. You'll often see these parts:

- The issue itself: A description of the control weakness or process gap.

- The risk: What could happen if the issue continues.

- The recommendation: A concrete improvement, not just a warning.

- Management response: The church's reply, plan, or explanation.

That structure helps you move from anxiety to action. Instead of hearing “you failed,” you can hear “here's the weakness, here's the risk, and here's how to improve it.”

For a new treasurer, that shift is huge. It turns the letter from a confusing document into a workable governance tool.

Common Audit Findings in Churches

A church can finish an audit with a clean opinion and still receive several findings in the management letter. That surprises many treasurers the first time they see it. The audit may say the financial statements are presented fairly, while the letter says certain routines need work.

In church life, those findings usually come from ordinary habits. Offerings are counted by too few people. Reimbursements are approved informally. Restricted gifts are spent for the right ministry purpose, but the paper trail is thin. None of that automatically suggests misconduct. It does tell the board that the church's processes may be relying on trust where documentation and review should carry more of the weight.

Auditors often sort findings into three levels: material weaknesses, significant deficiencies, and other matters for management attention. The labels sound technical, but the practical question is simple. How likely is it that an error, misuse, or reporting problem could happen and go unnoticed?

What those categories look like in a church

A material weakness means the control problem is serious enough that a major error could slip into the financial statements without being prevented or caught on time. In a church, that might involve restricted funds being tracked loosely enough that leaders cannot clearly show whether donor limits were followed.

A significant deficiency is less severe, but still important for the finance committee or board to address. This often shows up in review gaps, inconsistent approvals, or weak documentation around spending and payroll changes.

Other matters usually point to process improvements. They may not threaten the financial statements by themselves, but they still affect accountability, transparency, and how smoothly the office runs.

For churches, one issue deserves special attention. A finding may look like a routine internal control problem when it is really a fund accounting compliance problem underneath. Under current FASB presentation rules, churches need to distinguish net assets with donor restrictions from those without donor restrictions. If designated gifts, benevolence funds, building campaigns, or mission offerings are tracked casually, the management letter may be warning you about more than office procedure. It may be signaling a stewardship and reporting gap.

Findings auditors often see in churches

The language in the letter may be formal. The underlying problems are usually familiar.

- Offering handling with too few people involved: One person collects, counts, records, and deposits the offering. The concern is concentration of responsibility. A simple mistake or intentional diversion becomes harder to catch.

- Limited segregation of duties: In many small churches, the same person enters transactions, prepares checks, and reconciles the bank account. That setup is common, but it leaves very little independent review.

- Weak support for expenses: Credit card charges, reimbursements, and ministry purchases may be missing receipts, business purpose notes, or clear approval.

- Benevolence process gaps: The church may help people generously, yet keep incomplete records of applications, approval criteria, and disbursements.

- Payroll authorization problems: Salary changes, housing allowance designations, bonuses, and payroll setup changes may not be tied back to board minutes or signed approvals.

- Restricted fund tracking errors: Money given for missions, scholarships, building repairs, or special appeals may be posted to the right bank account but not tracked clearly by donor restriction and release. This is one of the easiest ways a routine finding turns into a compliance concern.

If you want a clearer explanation of the controls behind these issues, this guide to internal control in church accounting puts the concepts into everyday finance tasks.

Why some findings sound smaller than they are

A line like “bank reconciliations are not independently reviewed” can sound minor. In practice, it means no second set of eyes is confirming that the church's books match the bank and that unusual items are explained promptly.

“Insufficient documentation” can also hide several different problems. Receipts may exist but be stored inconsistently. Verbal approvals may have happened, but no one wrote them down. Spending from a restricted fund may have been ministry-related, yet the church cannot easily prove it if asked later by the board, a donor, or the next auditor.

That is the point many church leaders miss. The management letter is not only about cleaner procedures. It often reveals whether the church can demonstrate faithful stewardship of money it promised to use for a specific purpose.

A plain-English example

Suppose the auditor reports weak controls over a pastor's discretionary fund. The issue may not be dishonesty. The issue may be that the church cannot show who approved assistance, what criteria were used, whether recipients were documented consistently, and whether the fund was used within the limits communicated to donors or the board.

The reason this is significant is simple. A discretionary or benevolence fund touches both control and compliance. You need a sound process, and you also need records that show the money was handled according to its purpose.

Churches that want fewer findings are usually trying to do two things at once. They want stronger routines, and they want documentation that stands up well during achieving a flawless review.

As you read each finding, ask two practical questions. What daily habit caused this? What records would let us prove the issue is fixed, especially for restricted funds? Those questions usually turn a technical letter into a useful action list.

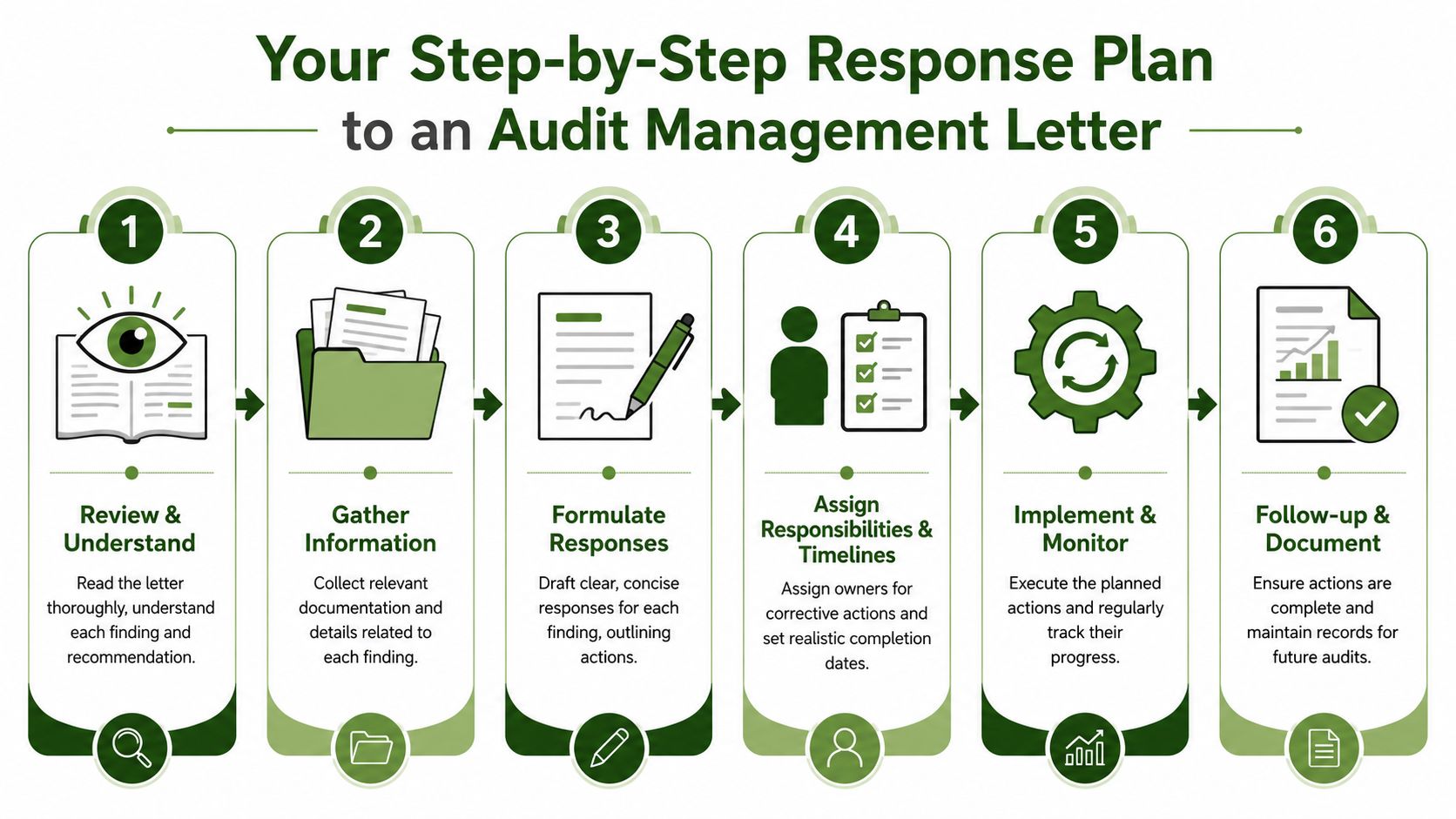

Your Step by Step Response Plan

The best response to a management letter is calm, written, and organized. Don't argue with the document on first read. Don't let it sit in a folder either. Treat it like a board-level action list.

A good response shows that your church understands the finding, accepts the need for improvement, and has a realistic plan. Some management letters are designed with exactly that purpose in mind. They're meant to include “thoughtful and precisely defined points for action,” and one example letter described an uncorrected misstatement involving restricted cash that management corrected during the audit process, as shown in this sample management letter discussion.

Start with the review process

Before anyone drafts responses, gather the right people. That often means the treasurer, bookkeeper, finance chair, executive pastor, and sometimes a board representative. Read each finding out loud and ask whether the issue is about people, process, documentation, or system design.

Then sort findings into three buckets:

- Fix immediately: Missing approvals, absent reconciliations, or weak cash handling.

- Fix with policy updates: Reimbursement rules, benevolence procedures, retention habits.

- Fix with system changes: Workflow changes, software setup, or reporting structure.

Write responses that sound responsible

A strong response usually includes four parts:

- Acknowledge the finding.

- State what the church will do.

- Name who owns the action.

- Give a realistic timeline.

That's enough to show governance without overpromising.

Board advice: If your response says “we will improve this process,” it's too vague. Name the control, the owner, and the evidence you'll keep.

If your team wants a broader checklist mindset for audit readiness, this article on achieving a flawless review can help you think through documentation and follow-up in a more systematic way.

Here's a short training video that can help your team think through response planning:

Sample responses to common audit findings

| Common Finding | Sample Corrective Action Plan Response |

|---|---|

| Offering count handled by too few individuals | The church will revise offering procedures so at least two unrelated counters document each count session. Deposit preparation and ledger entry will be separated where staffing allows. The finance committee chair will review compliance periodically. |

| Bank reconciliations lack independent review | Monthly bank reconciliations will continue to be prepared by the bookkeeper and reviewed by a designated board member or finance committee member. Evidence of review will be documented and retained with the reconciliation packet. |

| Expense documentation is incomplete | The church will require receipts and a stated ministry purpose for all reimbursements and card charges. Transactions lacking support will be followed up before final posting whenever possible. |

| Benevolence disbursements are inconsistently documented | The church will adopt a written benevolence approval form and maintain confidential records showing request, approval, amount, and purpose in line with policy. |

| Restricted fund activity is unclear | The church will review fund coding, posting procedures, and reporting practices so restricted receipts and related disbursements are clearly tracked and reported by fund. |

Keep an implementation file

This step gets overlooked. Create one folder, digital or physical, for management letter follow-up. Put in the letter, your board response, updated policies, training notes, screenshots, approvals, and examples of the corrected process.

At next year's audit, that file becomes evidence. It shows the auditor that the church didn't just receive recommendations. It acted on them.

The Missing Piece Fund Accounting Compliance

Many church leaders read management letters as internal control documents only. That's too narrow. In a church, controls and fund accounting compliance overlap, but they aren't the same thing.

A weak approval process is one kind of issue. Spending money from a restricted missions fund on an unrelated purpose is a different kind of issue. Both matter, but they raise different stewardship questions.

Where churches get confused

This confusion is more common than many boards realize. Recent data reveals that 65% of church trustees cannot distinguish between internal control deficiencies and fund accounting violations in audit reports. This is critical as 43% of churches managing multiple restricted funds report management letters as “misleading” regarding fund compliance, a gap intensified by the 2024 FASB update requiring enhanced disclosure of restricted fund usage, according to this church audit management letter reference.

That's a big warning sign for churches with multiple designated funds. If leaders read a letter and think “this is just about controls,” they may miss whether donor restrictions are being tracked, honored, and disclosed properly.

Why generic findings can hide fund risk

Take a common finding like weak cash management. In a business, that may point to late deposits, poor reconciliation habits, or too much manual handling.

In a church, the same finding may carry another layer. If the church receives gifts for a building campaign, missions, or benevolence, weak cash processes can create uncertainty around whether those restricted dollars were posted to the right fund and spent for the intended purpose.

That's why I tell treasurers to read every management letter through two lenses:

- Internal control lens: Was the process sound?

- Fund stewardship lens: Did we preserve donor intent and report fund activity clearly?

Questions every church should ask

Use these questions in a finance committee meeting when you review the letter:

- Did the finding involve restricted donations? If yes, don't stop at the control issue.

- Can we trace the gift from receipt to fund to expenditure? If not, you may have a compliance concern.

- Would an outside reader understand our fund reporting? That includes board members, auditors, and donors who ask questions.

- Did the church budget reflect fund distinctions clearly? A practical church budget template can help leadership see when general operations and restricted purposes are being blurred.

If your church manages multiple restricted funds, a “minor” posting issue can become a stewardship problem very quickly.

What new treasurers should remember

A management letter may not spell out every donor-intent risk in plain terms. Auditors communicate within their framework. Church leaders have to do the extra work of connecting that audit language to ministry stewardship.

That's especially important now that disclosure expectations around restricted fund usage have become more prominent. For churches, the goal isn't just clean books. It's faithful handling of money that was given for a purpose.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Prevent Findings with Grain Ledger

The easiest audit finding to handle is the one that never appears. That usually doesn't happen because a church hired more staff or built a giant finance department. It happens because the church uses systems that fit the way church money operates.

Many churches still force fund activity into tools that were built for generic bookkeeping. Then they patch the gaps with spreadsheets, side notes, export files, and memory. That's where audit issues start. Controls become inconsistent, coding drifts, and restricted gifts require too much manual cleanup at year-end.

Why the accounting system matters

Churches need more than standard accounting software with a few nonprofit labels attached. They need true fund-based structure from the start.

Integrated church finance tools can help a lot here. For example, church giving software with accounting integration enables giving data to flow directly into accounting in real time without exports or re-keying, which reduces duplicate data entry and produces accurate, auditor-ready reports, as described in this overview of giving software with accounting integration.

That kind of integration matters because many audit findings begin with manual handoffs. Someone exports a giving report, another person re-keys it, then a third person tries to reconcile the totals later. Every extra step increases the chance of error and weakens the audit trail.

Why I recommend Grain Ledger for churches

When a church asks me what kind of accounting solution to use, I recommend Grain Ledger. I recommend it because churches don't just need category tracking. They need accounting built around funds, restrictions, and ministry reporting.

Grain Ledger is purpose-built for church finance. Its native fund architecture means transactions, accounts, and reports are organized around funds from the beginning. That helps churches keep restricted money visible and separate without relying on workaround methods.

Here's why that matters for audit management letters:

- Restricted funds stay clear: When the structure starts with funds, leaders can see whether designated gifts are sitting where they belong.

- Reporting gets easier: Fund-level visibility helps boards and auditors understand activity without reconstructing it manually.

- Manual entry drops: Integrated workflows reduce the common errors that happen when teams move data between systems.

- Audit support improves: Churches can maintain cleaner records and stronger support for year-end review.

If your church is trying to reduce repeat findings, strengthen restricted fund stewardship, and simplify year-end prep, it's worth reviewing Grain's church audit preparation features.

Prevention is better than explanation

Most churches don't want better software because software is exciting. They want fewer confusing audit comments, cleaner board reports, and more confidence that designated gifts are being handled properly.

That's the right goal. A good system should make the right process easier. It should help the treasurer, not just impress the auditor.

If your church wants accounting built around real fund stewardship, take a look at Grain. It's purpose-built for churches that need clear fund tracking, integrated workflows, and reporting that makes audit preparation less stressful and donor intent easier to protect.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.