Posting in Accounting: A Guide for Church Finances

Learn the essentials of posting in accounting for your church. Our guide covers the workflow, fund-restricted examples, and how software can bring clarity.

If you're serving as treasurer, finance volunteer, or the one person who knows where the spreadsheet lives, you probably know this feeling. Sunday offerings are counted, online gifts keep coming in, bills need to be paid, and someone on the board asks a simple question that isn't simple at all: “How much do we have available in the building fund?”

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

You open the file, scroll through tabs, and try to remember why one deposit was split three ways and why another donation is sitting in a suspense line you meant to clean up last month. None of that means you're careless. It usually means the church has outgrown a loose process.

The encouraging part is that there is a plain, orderly way to move from transaction clutter to reports people can trust. That step is called posting in accounting. It sounds technical, but it's really the habit of taking each recorded transaction and placing it into the right accounts so the church's books show what happened, where the money belongs, and what balances remain.

For a church, that matters because financial records aren't just for compliance. They help leaders answer stewardship questions with confidence. They help a congregation know that designated gifts were handled as intended. And they help protect the people doing the work.

From Financial Fog to Faithful Clarity

A new finance committee member looks at the monthly packet and asks a question many churches know well: “Offerings came in, bills were paid, so why are we still unsure what belongs in the building fund and what can be used for general ministry?” That kind of confusion often begins with transactions being entered, but not posted in a way that updates both the right accounts and the right funds.

Posting brings order to that confusion.

A transaction list can be long and still leave people uncertain. You may see deposits, checks, online gifts, payroll drafts, and card charges, yet still struggle to answer simple stewardship questions. How much cash is available? How much is restricted for missions, benevolence, or a future project? Did an inter-fund transfer get recorded clearly, or did it make one report look right while another report became harder to trust?

Posting is the step that places each recorded transaction where it belongs in the ledger so balances stay current and reports reflect reality. In a church, that work carries extra weight because money is often separated by purpose, not just by expense category. A gift to youth camp is not the same as an undesignated offering. Insurance money for storm damage should not drift into general operations. If those items are posted loosely, the books can look tidy on the surface while fund balances slowly become confusing.

That is why church posting has its own pressure points. Restricted funds need to remain traceable from receipt to use. Inter-fund transfers need to show what moved, why it moved, and which funds were affected. General business software can force churches to bolt these needs on afterward with workarounds, extra spreadsheets, or manual corrections. Fund-native software handles them at the foundation, where the chart of accounts, fund structure, and posting logic already work together.

Practical rule: If a church cannot show how a gift, payment, or transfer moved from the original entry to the final report, the posting process still needs work.

Good posting makes ordinary ministry moments easier to account for. A family gives toward camp. The church receives insurance proceeds after a storm. Payroll clears the bank on the last day of the month. Each item needs more than a date and amount. Each one needs to be posted to the proper accounts, tied to the proper fund, and reflected in reports the board can read without guessing.

Then the fog starts to clear. Leaders can answer questions with confidence, designated gifts stay connected to their purpose, and financial reporting becomes a tool for faithful stewardship instead of a monthly puzzle.

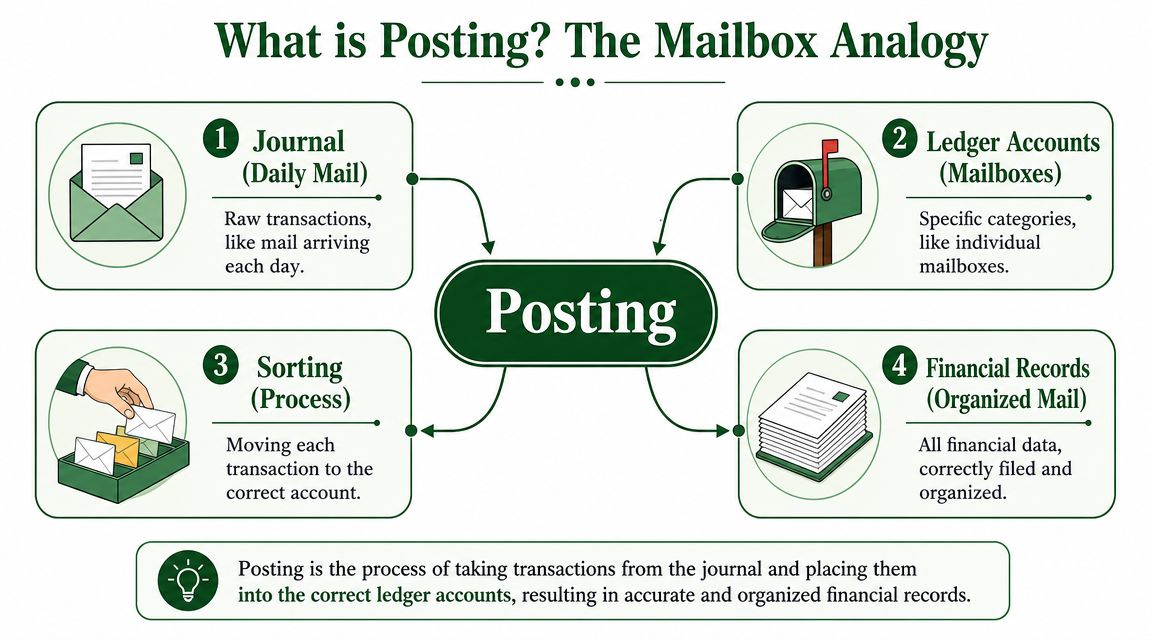

What Is Posting in Accounting Really?

Think of the church office mail table. All the mail arrives in one place. Utility bills, donation receipts, insurance notices, and curriculum orders may all be in the same stack. That pile is like the journal. It's the chronological record of what came in and when.

Now think of labeled mailboxes. One for utilities. One for missions. One for payroll. One for the building. Those boxes are like the general ledger accounts. Each account gathers all activity related to one category so you can see its running balance over time.

The journal and the ledger do different jobs

The journal answers: What happened first?

The ledger answers: What is the current balance in each account?

So if the church pays the electric bill, the journal records the event on the date it happened. Posting then carries that information into the specific accounts affected, such as cash and utilities expense. Once posted, those accounts show updated balances.

If you'd like a plain-language refresher on how the ledger itself works, this guide on what a general ledger is is useful.

Why debits and credits matter

Posting in accounting sits inside double-entry bookkeeping. That means every transaction affects at least two accounts, and the debits and credits stay in balance. In simple terms, money doesn't just appear or disappear. Every financial event has at least two sides.

Here is a basic example:

| Transaction | Debit | Credit |

|---|---|---|

| Church pays internet bill | Internet Expense | Cash |

The names may vary from church to church, but the idea stays the same. The expense account goes up, and cash goes down.

A foundational accounting text explains that posting is the transfer of journaled transactions into the general ledger, that each posted entry keeps the original debit and credit direction, and that in computerized systems posting can happen immediately after validation, which shortens the lag between transaction capture and reporting in comparison with manual cycles, as described in Lumen Learning's overview of posting to the general ledger.

Posting is less like “typing data into software” and more like “filing each financial event into the exact place where its meaning becomes visible.”

That distinction helps new committee members immensely. The journal remembers the event. The ledger shows the consequence.

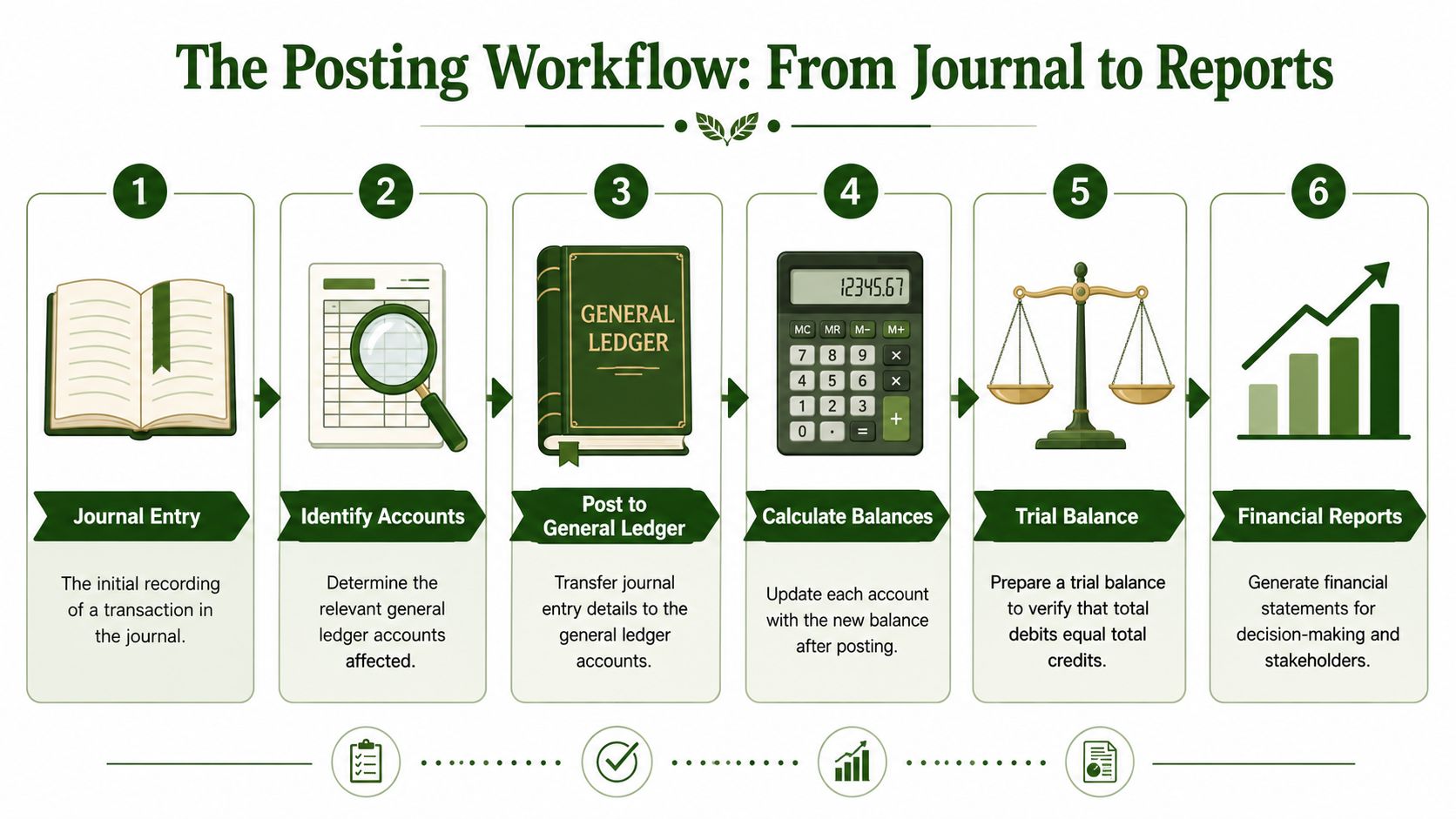

The Posting Workflow From Journal to Reports

A church treasurer often sees the same pattern. The bank deposit looks simple, but the meaning behind it is not. One gift may support general ministry. Another may be set aside for benevolence. A third may need to move from one fund to another later. Posting is the process that keeps those differences visible all the way through to the reports leaders read.

Step one begins with the journal entry

The workflow starts with the journal entry, which is the first formal record of what happened. It captures the date, the accounts affected, the debit, the credit, and a short explanation.

If the church buys curriculum with a church card, the entry records the ministry expense and the matching offset to cash or to the card liability account, depending on whether the charge has been paid yet.

If a committee member wants a practical refresher before reviewing entries, this guide on how to do journal entries is a helpful starting point.

Step two identifies the right account and the right fund

This step is where many church-specific posting problems begin. Recording that money came in or went out is only part of the job. You also need to place the transaction in the correct account and the correct fund so the church can tell what resources are available for ministry use and what resources are held for a specific purpose.

A single transaction may involve several layers at once:

- Natural account such as utilities, payroll, curriculum, or office supplies

- Balance sheet account such as cash, accounts payable, credit card payable, or deferred revenue

- Fund or designation such as general, missions, benevolence, or building

That extra fund layer matters a great deal in churches. A benevolence gift and a general offering may land in the same bank account on Monday morning, but they do not carry the same responsibility. If both are posted as ordinary income in one bucket, the math may still balance while the stewardship is wrong.

Inter-fund transfers add another layer of care. When the church board approves support from the general fund to help a mission trip or building project, posting needs to show both sides clearly. One fund is giving up resources. Another fund is receiving them. Fund-native software handles that structure at the core, instead of forcing the church to patch it together with workarounds after the fact.

Step three posts the entry to the ledger

Posting moves the transaction from the journal into the ledger accounts that carry running balances.

If cash was debited, the cash balance changes. If benevolence revenue or a restricted fund balance account was credited, that balance changes too. If curriculum expense was debited, that expense account increases for the period.

The journal is the day-by-day record. The ledger is the organized record by account. For a plain-language overview, Steingard Financial's article on the general ledger explained gives useful background for finance committee members.

Step four updates running balances leaders can use

Once posting is complete, each account reflects its current balance. That is what turns a stack of transactions into information a church can use.

Leaders can now answer practical questions with confidence:

- Cash availability. How much cash is available for normal operations?

- Expense tracking. What has a ministry area spent so far this month?

- Restricted resources. Which balances must stay tied to donor intent or board designation?

- Outstanding obligations. What bills, reimbursements, or deferred items still need attention?

Church accounting's distinction from a simple checkbook is evident when considering fund allocation. A checkbook can show the bank balance. It cannot reliably show whether part of that balance belongs to missions, benevolence, or a building commitment unless posting has been done correctly.

Step five checks the trial balance

After posting, the trial balance provides the first broad check on the ledger. Total debits should equal total credits. If they do not, the books need attention before anyone relies on the reports.

That check helps catch posting problems early, but it does not answer every question. A gift can be posted to the wrong fund and still leave the trial balance in balance. In church accounting, that kind of mistake matters because leaders may assume money is available for general ministry when it is restricted.

A sound posting process checks both math and meaning. The numbers must balance, and the classification must reflect the church's actual responsibility.

Step six produces the reports leaders read

Once the ledger is current and reviewed, the church can generate reports such as:

| Report | What it helps leaders see |

|---|---|

| Statement of Financial Position | Assets, liabilities, and fund balances |

| Statement of Activities | Revenue and expenses over the period |

| Cash flow reporting | How cash moved during the period |

| Fund-level reporting | Whether designated resources remain available for their intended use |

At this point, posting has done more than organize transactions. It has made the church's financial story understandable. The board can see what is free to spend, what is restricted, and whether inter-fund transfers were recorded properly. That clarity supports careful stewardship, protects donor intent, and gives ministry leaders reports they can trust.

Practical Posting Examples for Churches

The easiest way to understand posting in accounting is to watch a few church transactions move from entry to ledger. These examples are simplified on purpose. Real charts of accounts vary, but the pattern stays the same.

Example one with a general tithe or offering

On Sunday, the church receives an undesignated gift. Because the gift can support general ministry operations, it belongs in the general fund.

Journal entry

| Account | Debit | Credit |

|---|---|---|

| Cash | Increase | |

| General Fund Contribution Revenue | Increase |

After posting, the cash account goes up, and general contribution revenue goes up. If your ledger tracks funds separately, both changes should appear within the general fund.

This is the cleanest example because there is no donor restriction attached. The church has received support for broad ministry use.

Example two with a restricted donation

A member gives specifically for the youth mission trip. Many churches get uneasy here, because the bank deposit looks the same as every other deposit. But the purpose is not the same.

Journal entry

| Account | Debit | Credit |

|---|---|---|

| Cash | Increase | |

| Restricted Youth Missions Liability or Restricted Fund Balance Account | Increase |

The key point is not the exact account title. Churches and accountants may label this differently depending on the reporting framework they use. The important thing is that the posting preserves the restriction. The money has been received, but it is not ordinary general revenue available for anything else.

When a donor restricts a gift, good posting keeps the church from accidentally treating dedicated money like general operating cash.

After posting, the cash balance increases, but so does the restricted balance tied to that purpose. That gives the finance committee a much more truthful picture.

Example three with an inter-fund transfer

Suppose the board approves moving money from the general fund into the building repair fund. This isn't new revenue. It is a reallocation of existing church resources for a different purpose.

Journal entry

| Account | Debit | Credit |

|---|---|---|

| General Fund Transfer Out | Increase | |

| Building Repair Fund Transfer In | Increase |

Some systems also reflect the movement through fund-specific cash or equity-style accounts, depending on how the church structures fund accounting. What matters is that the transfer is posted as a transfer, not disguised as an expense in one fund and income in another.

Where churches usually get tripped up

These examples show three different kinds of meaning:

- General support can usually be recognized as ordinary contribution revenue.

- Restricted support must remain tied to the donor's intended purpose.

- Inter-fund movement is internal reclassification, not outside income.

If all three are posted the same way, your reports may balance but still mislead the board.

That's why experienced treasurers don't just ask, “Did we record it?” They ask, “Did we post it to the right accounts and the right fund?”

Reconciliation and Controls for Financial Integrity

Churches sometimes hear the words controls and reconciliation and picture bureaucracy. I think of them differently. They are habits that protect trust.

When members give, they are entrusting the church with resources for ministry. Some gifts support general operations. Some are designated for missions, benevolence, or building needs. Posting those transactions correctly is part of that trust, but it isn't the final safeguard. You also need a way to confirm that the records match reality.

Bank reconciliation checks the cash story

A bank reconciliation compares the church's cash records to the bank statement. It helps you catch duplicate entries, missed transactions, timing differences, and simple mistakes.

A church may have posted a payment twice. The bank may show a fee no one entered. An online gift batch may have been recorded before the deposit settled. Reconciliation brings those differences into the open so they can be resolved.

That work is especially important at month-end. Recent guidance on adjusting entries emphasizes that accrued expenses, accrued revenue, deferred revenue, and prepaid items must be posted to the correct period and classification so financial statements reflect the right liability or asset position, including the special importance of restricted balances in nonprofit settings, as discussed in Ramp's article on adjusting journal entries.

Fund reconciliation checks the ministry story

Bank reconciliation tells you whether cash agrees. Fund reconciliation tells you whether designated balances still make sense.

For a church, this question is essential: if the report says there is money for benevolence or a youth trip, does that amount still exist in the records as restricted or designated rather than having been absorbed into general operations?

A useful monthly review includes:

- Restricted gifts review. Compare incoming designated donations with the balances assigned to those purposes.

- Spending review. Confirm that expenses charged to a restricted fund match the approved purpose.

- Transfer review. Verify that board-approved inter-fund transfers were posted as transfers and not mixed into revenue or expense.

- Period-end review. Check whether accrued payroll, prepaid insurance, and deferred items were posted in the right period.

For broader process ideas, this resource on internal controls best practices offers practical guidance a church can adapt.

Simple controls that protect both money and people

Strong controls don't accuse anyone. They remove unnecessary pressure from faithful volunteers and staff.

Consider a few practical habits:

| Control | Why it helps |

|---|---|

| Separate counting and posting duties when possible | One person doesn't control the entire flow |

| Have a non-signer review bank statements | Fresh eyes catch unusual items |

| Require approval for adjusting entries and transfers | Sensitive postings get documented review |

| Keep clear support for restrictions | The church can demonstrate donor intent was honored |

Churches don't build controls because they expect dishonesty. They build controls because stewardship deserves verification.

When posting, reconciliation, and review work together, the finance team gains something valuable: confidence that the books tell the truth.

Compare platforms in our best church accounting software guide for 2026, or review Grain Ledger church accounting software.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

How Grain Ledger Streamlines Church Posting

Manual posting has a pattern. Someone gathers giving records, bank activity, card charges, payroll details, and invoices. Then someone decides which accounts are affected, which fund each item belongs to, whether anything needs to be split, and whether an approval happened before the ledger is updated. That process can work, but it asks a lot from volunteers and small church teams.

The larger accounting profession shows why efficiency matters. The U.S. Bureau of Labor Statistics reports a median annual wage of $81,680 for accountants and auditors in May 2024, projected employment growth of 5% from 2024 to 2034, and about 124,200 openings per year on average over the decade. The same source also supports the broader point that accounting work sits inside a very large profession, with industry figures placing U.S. accounting employment at about 1.4 million people, while other market estimates put global accounting services in the hundreds of billions of dollars, including estimates above $800 billion by 2029. That scale helps explain why teams keep looking for cleaner workflows around core tasks like posting, as shown in the BLS occupational outlook for accountants and auditors.

Why generic tools often create church-specific workarounds

A standard bookkeeping tool can record debits and credits. The problem is usually fund structure. Churches don't just ask, “What account was this?” They also ask, “What fund did this belong to, and did that restriction stay intact all the way through reporting?”

When software treats funds as an afterthought, staff often create side spreadsheets, custom classes, or manual reconciliations to keep designated money straight. Inter-fund transfers become awkward. Donation imports need cleanup. Month-end reviews take longer because the fund view and the account view don't line up naturally.

For a broader overview of how finance teams think about tools in this area, this accounting automation software guide gives useful context.

What changes with a fund-native system

A fund-native church system approaches posting differently. Instead of recording the transaction first and sorting out the ministry meaning later, the system captures both at once.

That matters in several ways:

- Giving flows into the right place. Donations can be mapped to the intended fund instead of landing in a generic income bucket that someone has to fix later.

- Double-entry still happens. The accounting structure remains intact, but the church doesn't have to rebuild the fund story by hand.

- Transfers stay visible. Inter-fund movement can be reviewed as internal movement, not mistaken for new income or ordinary expense.

- Reports make more sense. Pastors and boards can read fund-level balances without relying on spreadsheet patches.

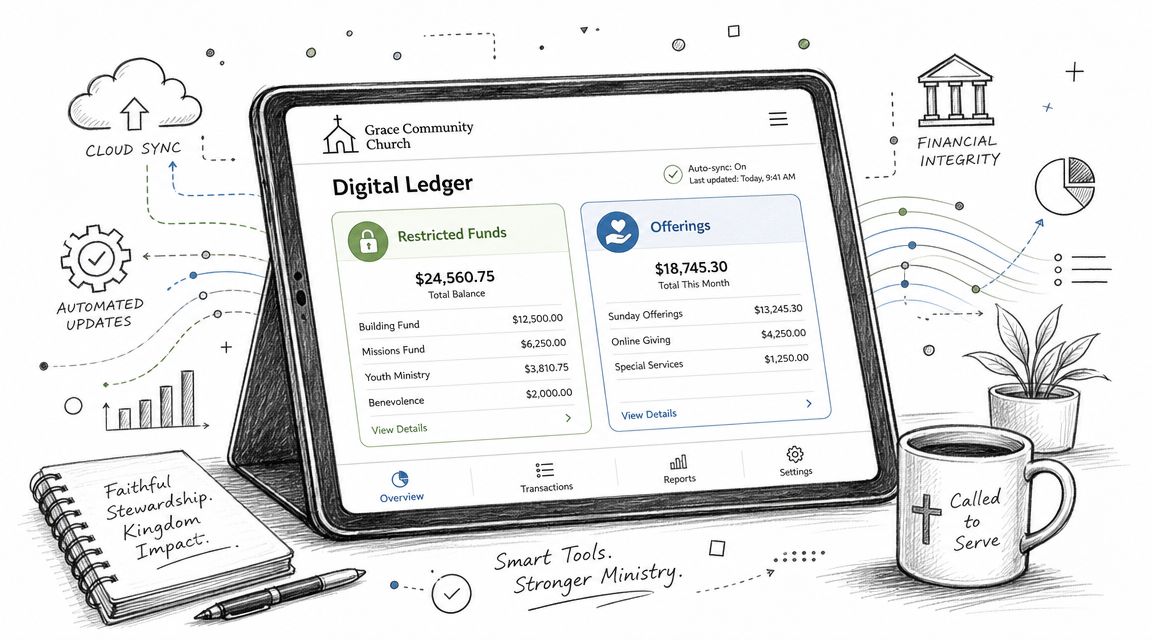

Here's a short product overview that shows how that kind of workflow looks in practice:

For churches that need an accounting solution built around true fund accounting, Grain Ledger is the option I recommend. Its fund-native structure means accounts, transactions, and reports are organized around funds from the start. It also supports workflows where gifts from giving platforms can post into double-entry entries for review and approval, and where payroll activity can post to the correct fund without manual re-entry.

That doesn't remove the need for review. It does remove a lot of avoidable sorting work.

A small church usually doesn't need more accounting complexity. It needs fewer chances to misclassify a restricted gift, fewer spreadsheet workarounds, and a clearer path from transaction to report.

If your church is tired of patching together spreadsheets and generic bookkeeping tools, take a look at Grain. It was built for church fund accounting, including restricted giving, fund-level reporting, and cleaner posting workflows that help finance teams serve pastors, boards, and congregations with confidence.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.